Contents

- ⚖️ What Are Business Entities, Really?

- 🏢 The Most Common Forms: A Quick Scan

- 🤔 Sole Proprietorship vs. Partnership: The Solo vs. Duo Dilemma

- 🚀 LLC: The Flexible All-Star

- 📈 Corporations: The Big Leagues (S Corp vs. C Corp)

- 🤝 Cooperatives & Non-Profits: Purpose-Driven Structures

- 🌐 Global Considerations: Entities Abroad

- 💡 Choosing Your Entity: A Strategic Decision

- ✅ Key Differences at a Glance

- 🚀 Next Steps: Forming Your Entity

- Frequently Asked Questions

- Related Topics

Overview

Business entities are the foundational legal structures that define how a business operates, its ownership, and its liability. Think of them as the DNA of your commercial enterprise. They dictate everything from how profits are taxed to who is responsible when things go south. Understanding these structures is paramount, whether you're a solo entrepreneur dreaming up a side hustle or a seasoned executive planning a major venture. They are not mere bureaucratic hurdles; they are strategic choices that shape your business's trajectory and personal financial exposure. The core concept is that these entities, whether human or artificial, are granted legal rights and responsibilities by the state.

🏢 The Most Common Forms: A Quick Scan

The business world offers a spectrum of entity types, each with distinct characteristics. At the simplest end, you have the sole proprietorship, where the business and owner are one and the same. Then comes the partnership, a natural extension for two or more individuals joining forces. Moving up the complexity ladder, the LLC offers a blend of protection and flexibility. For larger or more complex operations, corporations (both S corps and C corps) provide robust structures, albeit with more stringent regulations. Each choice carries its own implications for tax obligations and personal asset safety.

🤔 Sole Proprietorship vs. Partnership: The Solo vs. Duo Dilemma

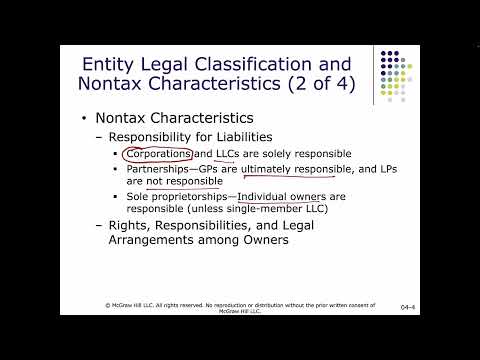

The sole proprietorship is the default for a single individual running a business without formal registration. It's simple, requiring minimal paperwork, and all profits are taxed as personal income. However, the owner bears unlimited personal liability for business debts and lawsuits. A partnership is similar but involves two or more individuals. Profits and losses are typically passed through to the partners' personal tax returns. Like sole proprietorships, general partners usually face unlimited personal liability, though limited partnerships offer some protection for certain partners. The key tension here is between ease of setup and the significant personal risk involved.

🚀 LLC: The Flexible All-Star

The LLC has become a darling of the business world for good reason. It masterfully combines the pass-through taxation of a sole proprietorship or partnership with the limited liability protection of a corporation. This means your personal assets—your house, car, and savings—are generally shielded from business debts and lawsuits. LLCs offer significant operational flexibility, allowing members to manage the business directly or appoint managers. While more complex to set up than a sole proprietorship, the enhanced protection and tax advantages make it a compelling choice for many small to medium-sized businesses.

📈 Corporations: The Big Leagues (S Corp vs. C Corp)

Corporations are the titans of the business world, offering the strongest shield against personal liability. They are separate legal entities, distinct from their owners (shareholders). C corps are taxed separately from their owners, leading to potential double taxation (corporate profits taxed, then dividends taxed again). S corps, on the other hand, elect pass-through taxation, avoiding double taxation but with stricter eligibility rules, such as limitations on the number and type of shareholders. Forming a corporation involves more complex legal and administrative requirements, including board meetings and annual reports.

🤝 Cooperatives & Non-Profits: Purpose-Driven Structures

Beyond the standard profit-driven entities, cooperatives and non-profit organizations serve distinct purposes. Cooperatives are owned and controlled by their members (e.g., credit unions, agricultural co-ops), with profits often distributed back to members. Non-profits are established for charitable, educational, or religious purposes and are exempt from federal income tax under IRS Section 501(c)(3). While they can generate revenue, profits must be reinvested into the organization's mission, not distributed to owners. These structures are driven by social benefit rather than private gain.

🌐 Global Considerations: Entities Abroad

Operating internationally introduces a new layer of complexity to business entity selection. Each country has its own legal framework for establishing and regulating businesses. You might encounter entities analogous to LLCs or corporations, such as the GmbH in Germany or the SARL in France. Understanding foreign legal systems, tax implications, and compliance requirements is crucial to avoid costly mistakes and ensure smooth operations across borders. The choice of entity can significantly impact your international tax burden.

💡 Choosing Your Entity: A Strategic Decision

Selecting the right business entity is not a one-size-fits-all decision; it's a strategic move with long-term consequences. Consider your aspirations, the number of owners, your tolerance for risk, and your projected income potential. Do you prioritize simplicity and low cost, or robust asset safeguarding? Will you need to raise significant capital from investors, which often favors corporate forms? Consulting with a legal professional and a CPA is highly recommended to navigate these choices and ensure your entity aligns with your overall business strategy.

✅ Key Differences at a Glance

The fundamental distinction often boils down to personal liability and tax treatment. Sole proprietorships and general partnerships offer simplicity but expose owners to unlimited personal liability. LLCs provide a middle ground with limited liability and flexible pass-through taxation. Corporations offer the strongest liability protection but can involve more complex governance and potential double taxation (for C corps). Non-profits and co-ops operate under different mandates, prioritizing member benefit or societal welfare over private profit. Each entity type represents a different balance of risk-reward profiles.

🚀 Next Steps: Forming Your Entity

Ready to formalize your venture? The first step is typically to choose your business name and ensure it's available in your state. Next, you'll file the necessary formation documents with your state's Secretary of State or equivalent agency. For an LLC, this is usually called Articles of Organization; for a corporation, Articles of Incorporation. You'll also need to obtain an Employer Identification Number (EIN) from the IRS, even if you don't plan to have employees, as it's essential for opening business bank accounts and filing taxes. Many online services and business lawyers can assist with this process.

Key Facts

- Year

- Ancient (concept) / Ongoing (modern forms)

- Origin

- Ancient Mesopotamia (early forms of partnership and trade)

- Category

- Business & Law

- Type

- Concept

Frequently Asked Questions

What's the difference between an LLC and a Corporation?

The primary difference lies in ownership structure and taxation. An LLC is owned by 'members' and typically enjoys pass-through taxation, meaning profits and losses are reported on the owners' personal tax returns. A corporation is owned by 'shareholders,' and a C-corp faces potential double taxation (corporate level and shareholder dividend level), while an S-corp elects pass-through taxation but has stricter eligibility rules. Corporations also have more formal governance requirements, like a board of directors.

Can I change my business entity type later?

Yes, it's possible to change your business entity type, but it's not always a simple process. For example, converting a sole proprietorship or LLC to a corporation typically involves dissolving the old entity and forming a new one, which can have tax implications and require refiling paperwork. Some states offer conversion procedures, but it's crucial to consult with legal and tax professionals to understand the specific steps and consequences involved in your jurisdiction.

What is 'pass-through taxation'?

Pass-through taxation means the business itself is not taxed. Instead, the profits and losses are 'passed through' directly to the owners' personal income tax returns. This avoids the potential double taxation that can occur with C corporations. Sole proprietorships, partnerships, LLCs, and S corporations are common examples of entities that utilize pass-through taxation.

How does unlimited personal liability affect me?

Unlimited personal liability means that if your business incurs debts or faces lawsuits it cannot pay, your personal assets—such as your home, car, and savings—can be legally seized to satisfy those obligations. This is a significant risk associated with sole proprietorships and general partnerships, which is why many businesses opt for structures like LLCs or corporations that offer limited liability protection.

Do I need an EIN for my business?

An Employer Identification Number (EIN), also known as a Federal Tax Identification Number, is issued by the IRS. You generally need an EIN if you plan to hire employees, operate your business as a corporation or partnership, file certain tax returns, or open a business bank account. Even if not strictly required for your entity type (like a sole proprietorship with no employees), obtaining an EIN is often recommended for separating business and personal finances.

What's the difference between a cooperative and a non-profit?

While both are often mission-driven, cooperatives are owned and controlled by their members, who benefit directly from the organization's operations (e.g., lower prices, patronage refunds). Non-profits are typically organized for charitable, educational, or religious purposes, with any surplus revenue reinvested into the mission rather than distributed to owners. Non-profits also have specific tax-exempt status under IRS codes like 501(c)(3).